In early 1985, change was in the air for the London Stock Exchange (LSE). For decades stockbrokers had charged a fixed scale of minimum commission, and the distinction between stockjobbers, who traded stock on their own account, and stockbrokers, who could act only as agents, had been rigidly enforced.

This system had proved robust, and had certain advantages. It aligned the brokers’ and clients’ interests – as there was no discussion about commission rates, brokers were incentivised to provide the best research and negotiate the best dealing price for their clients. As for the jobbers, being constituted as partnerships or unlimited liability companies, if they failed the owners were personally liable. As a result, risk was very carefully managed, and failures were rare.

But this modest appetite for risk was consigning the City of London to the second division of world equity markets. The Thatcher government had ambitions for London as a global financial centre: also, and not unreasonably, saw the minimum commission scale as a cosy cartel.

Cecil Parkinson, the Trade and Industry Secretary, had Margaret Thatcher’s backing to shake up the LSE. In 1983 he negotiated rule changes with Chairman Nicholas Goodison: the carrot was the continued growth of the LSE, and of London as a financial centre. The stick was the threat of being taken to the Restrictive Practices Court over commission rules.

By 1985, the LSE was ready to put forward detailed proposals to its members. The most important was that Member Firms (whether brokers or jobbers) could now be owned by a single non-member (in practice, a limited company). This would pave the way for the partners who owned the broking and jobbing firms to sell their firms to the big banks – mostly American or British – who wanted a foothold in the growing London market. Other changes included permitting member firms to take positions in stock, and abolishing the fixed commission scale. These changes, which became known as “Big Bang” would also introduce computerised, screen based trading, and soon lead to the end of the Stock Exchange trading floor.

***************

By now, my career was starting to take off. I had been at Gilbert Eliott (a broking firm) for over three years: I had passed the four parts of the LSE membership examination, and was bringing in new business for the Preference desk. It was becoming clear that members would be offered shares in exchange for their ownership of the LSE, and that these shares would be valuable: besides the value of the Exchange as a business, the LSE owned the Stock Exchange Tower at 125 Old Broad Street, 26 floors of prime London property.

My boss in the Preference Department was Robert Wild, a shrewd and patient mentor. Spotting an opportunity to provide a benefit to employees at no cost to the firm, he put me and our market dealer Roger forward to become Members. I was quite flattered by this: three years was the minimum period of service in an LSE firm to obtain membership, and I had only been there a few months longer than that. I was still a lowly “Blue Button”, allowed to check prices but not officially to deal. I was now in line for the coveted “Silver Button” which denoted Membership, bypassing the intermediate Yellow. Our applications were successful, and on 11th April 1985 Roger and I celebrated becoming LSE members.

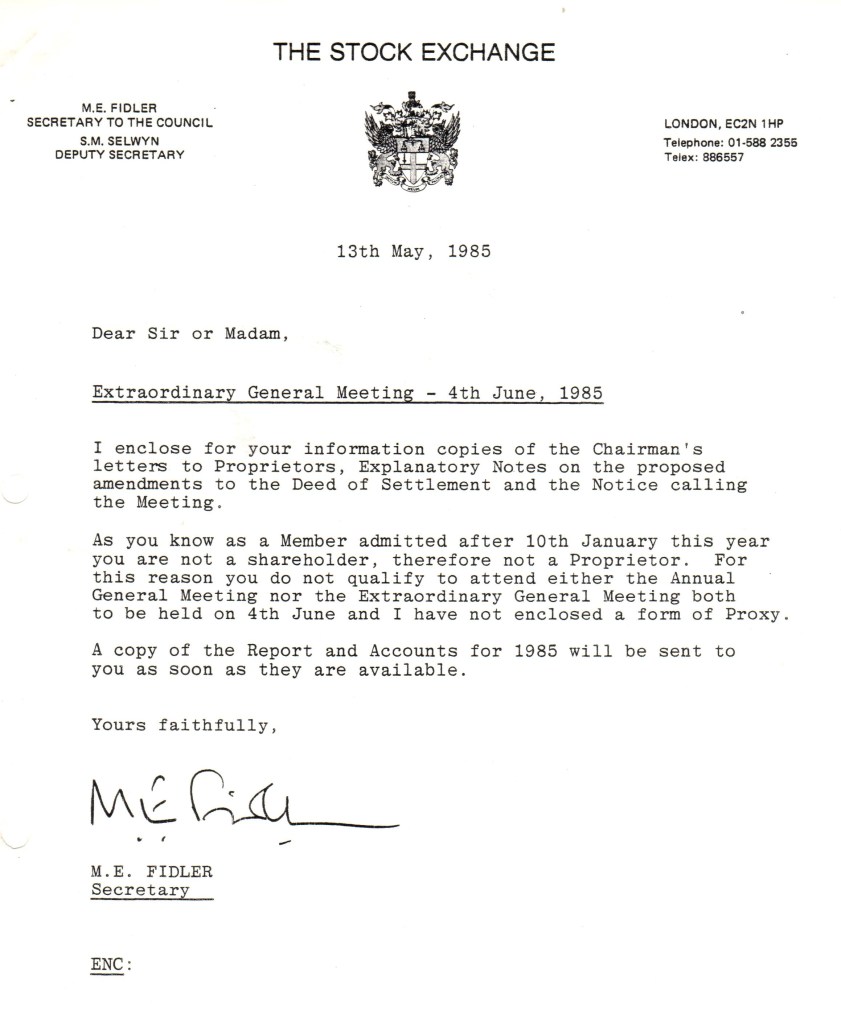

But there was a fly in the ointment. Once it became known that members’ shares would become transferable and saleable, the LSE feared “speculative distortions in the pattern of application for membership”. So they had ruled that any applicants after 10th January could still be granted membership, but would not receive a share or vote.

Roger and I weren’t happy about this. Gilbert Eliott weren’t famously generous employees, and the rumoured value of the new members’ shares was substantial. We didn’t like the idea of the door being slammed in our faces. But what could we do about it? Only try to kick up a fuss. I asked Robert Wild if he objected to our launching a campaign. He did not, although he quite reasonably asked that we should keep Gilbert Eliott’s name out of it – the firm was in the midst of delicate negotiations with a potential buyer, an Austrian bank called Girozentrale. Any whiff of scandal or trouble could have derailed the whole deal.

We obtained a list of the people who, like us, had been admitted to membership after January 10th, and circulated them all via the pigeonholes at the Stock Exchange with a letter – so incendiary that no copies survive – drawing attention to the injustice of the situation, and calling them to action: a call which was largely answered. Some contributed by writing strongly worded letters to the press and to Sir Nicholas Goodison.

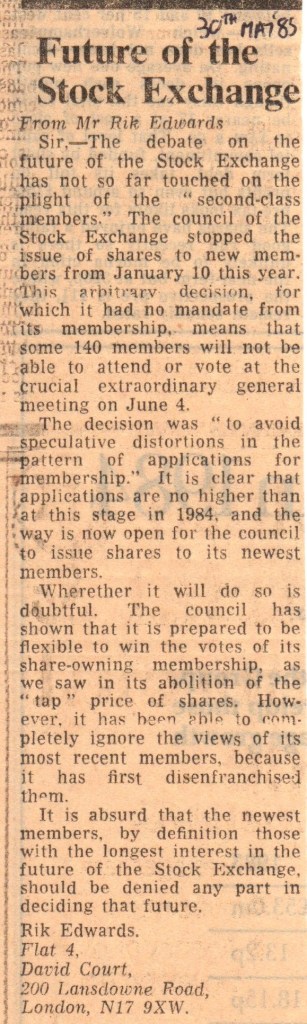

My effort was this letter to the Financial Times, which spawned a small news item in that newspaper, and soon afterwards the leading story in Financial Weekly:

Looking back, I feel some embarrassment about this campaign. An overpaid young man missing out on a bit of extra money was not the worst problem in the world. And my arguments are transparently self-serving: was I really concerned about having a say in the Stock Exchange’s future, or just annoyed to be missing out on a juicy payout? But we did feel a sense of injustice, and wanted to take some kind of action.

Our campaign had, I estimate, zero impact. As we had no votes, the Stock Exchange could happily ignore our opinion. If anything we might have persuaded some voting members to vote in favour of the Deed of Settlement before a bunch of new arrivals came in and diluted their shareholding.

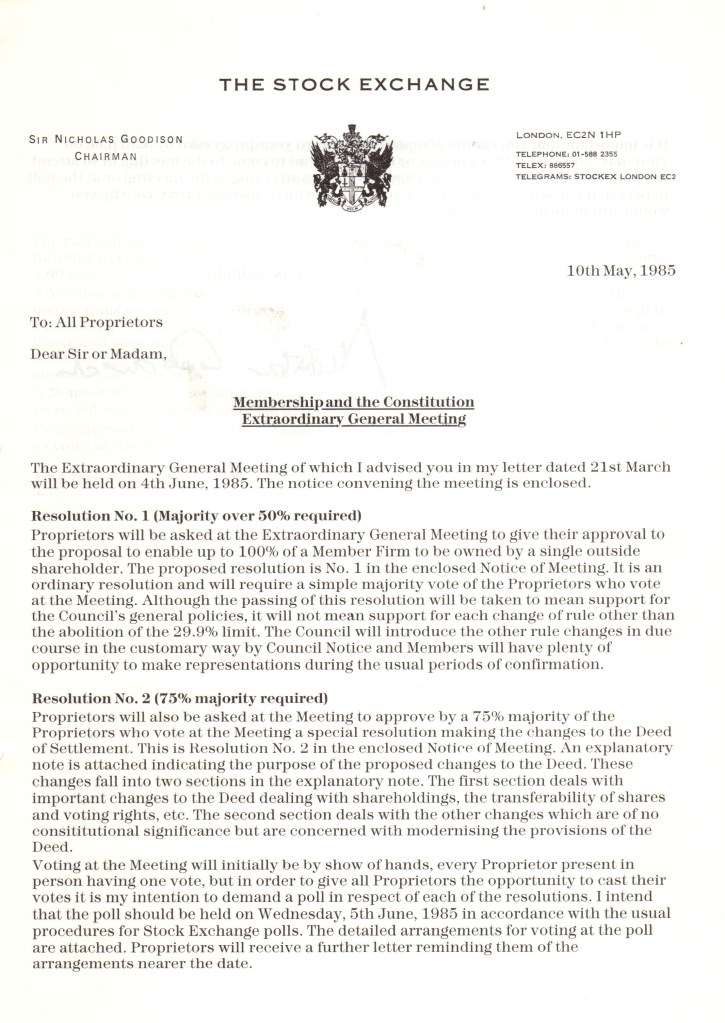

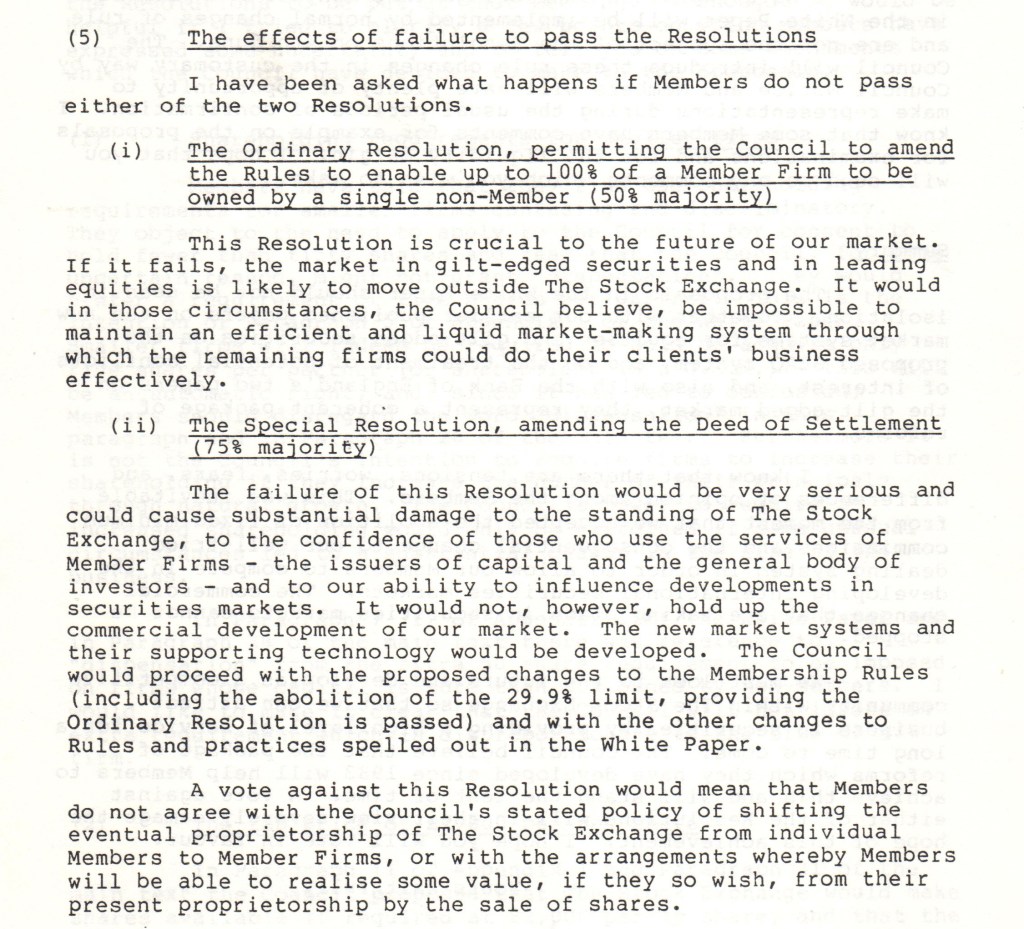

But the LSE and Sir Nicholas had much bigger problems to grapple with. Many members, especially those who had not achieved partner status in their firms, and members of smaller and provincial firms, felt that the changes were being rushed through on disadvantageous terms so that the partners in large firms could cash in. The Deed of Settlement vote required a 75% vote to pass, a high hurdle. Sir Nicholas made a determined case for a yes vote:

Anecdotal evidence had it that some of the larger firms, where partners had a great deal to gain from the proposals passing, were ruthless in pressuring their employees to vote in favour. One firm allegedly demanded that voting forms should not be posted direct, but returned to their secretary’s office – presumably so that the partners could check that people had voted the “right” way, and could bully or discipline those who had not. Imagine what the press would make of such behaviour in a trade union strike ballot.

Despite his urbane and charming personality, Sir Nicholas had become something of a hate figure among sections of the membership in the course of his attempts to implement change: some years later, when he became chairman of TSB Group, one colourful character went to the trouble of buying shares in the company, just so he could continue to harangue and heckle Goodison at meetings.

On June 4th I nervously turned on Channel 4 evening news (yes, this was national news) to hear the result of the vote. The Deed of Settlement vote had failed. Good news.

So the shares issued in exchange for membership rights would not after all be transferable. But we new joiners celebrated because one share was issued to each of us, and we now enjoyed the same rights as long established members. Our campaign may have had little impact, but we had arrived at our destination by a different route, thanks to the rebellious streak in a large minority of the voting membership.

Though I didn’t give it much thought at the time, my willingness to get involved in a battle might have hindered my career if I became known as a troublemaker. In retrospect, that might be why I spent my career mostly in challenger firms. I wasn’t made of the right stuff for the bigger, established firms.

The shares did turn out to be valuable, eventually. In 2000, as part of the London Stock Exchange’s proposal to become a listed company, they were repaid at £10,000 each. That certainly felt like a victory – even if we hadn’t earned it ourselves.

And Big Bang. Was it worth it? The LSE certainly saw very strong growth in business, and it did my career no harm. But some argue that it was part of a process where market participants grew larger, more interconnected and more sophisticated. They were then better able to insulate themselves from the consequences of their own poor credit decisions, by packaging up and selling risk in opaque and poorly understood securities. And that was a major cause of the 2008 Financial Crisis.

Leave a comment