In our family life, 1996 was a good year. Alice was born, and our first daughter, Rachel, was two, and growing up fast. We were adjusting to life in our house in Chorleywood, having moved from north London the previous autumn.

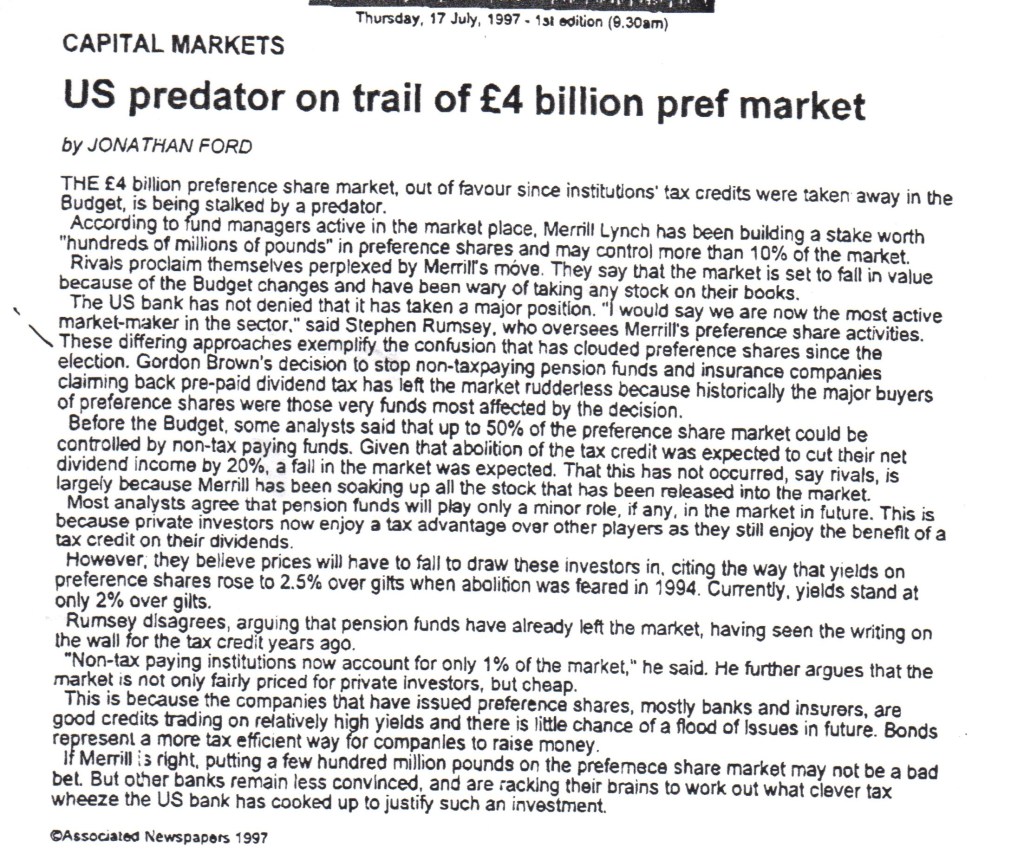

But at work, things weren’t going so well. Merrill Lynch, the “thundering herd”, had turned its mighty power on to my cosy little domain: UK preference shares. This had been a sleepy place with modest turnover and comfortable trading margins: enough to make a decent living for the handful of people who specialised in this niche area. It had run on knowledge and contacts, and capital had played a relatively small part.

However, Merrill Lynch had world domination in mind, and surprisingly the UK preference market was part of their plans. They may have been encouraged in this by the experienced group of fixed income salesman and traders they had recently recruited. Experienced and also wealthy: most, had already made serious money from selling their share of their previous employers – London broking and jobbing firms – to large banks desperate for a slice of the City, when it was opened up by the Big Bang in 1986. Also, of course, they had benefited from decades of generally lucrative employment.

Merrill may not have given much thought to the risk appetite of prosperous employees in their fifties, especially recent recruits with no particular company loyalty. Perhaps they should have done. Their team would have been on contracts that required a large lump sum payment in the event of redundancy. So they couldn’t lose: if they took a large gamble with Merrill’s money and won, they would get fat bonuses: if they lost, they would lose their job, bank a healthy payoff and stroll off into a comfortable retirement.

So their game was on. In the small number of preference shares with relatively large issue sizes, Merrill started to make hyper-competitive prices. For example, in Bank of Scotland 9 1/4% preference, where we would perhaps have guaranteed a client or broker a price in 100,000 or 250,000 in order to work a total order of half a million or more on a three point dealing spread, they might make a half point price in a million, sometimes as many as five million. So if, say, they made clients and brokers a price of 131.5 – 132 in one million, they were offering to buy up to a million shares at 131.5p, or sell up to a million at 132p. To put this in perspective, the whole share issue was only 200m – to make such a close price in such a large size was a huge commitment.

Our modus operandi of making a margin by negotiated trade was completely redundant, now that clients could instantly get their business done elsewhere in size and at close prices. As a relatively small firm, we didn’t have the capital to compete with Merrill’s pricing: nor did we think it sensible to try. We knew that providing this spectacular level of liquidity in such a small market was unsustainable in the long run. Although typically the City judges people in the short run.

On one occasion, after the new Chancellor Gordon Brown announced a tax change which was unambiguously bad for preference shares, Merrill continued to march their prices upwards. As they did so, naturally they acquired a further large amount of stock as investors deemed the shares unattractive to hold at the higher levels.

Within a few months, we had withdrawn from price making in the issues which Merrill dominated, although a couple of our competitors soldiered on. Business was very thin for a while: we were reduced to scratching around in the most arcane corners of our market to try to make a turn. There were days when we failed to book a single ticket or register any movement at all on our profit and loss account. Difficult times.

My personal life, although on its planned trajectory, didn’t help. The combination of lost sleep and the stress of being the unconfident father of a toddler and a baby meant I lacked the energy to reinvent my business to meet the competitive challenge. Also my daily commute had increased from half an hour when we lived in London to an hour and a quarter, which made it a long day.

In late 1998 some relief for us came from a newly fashionable capital instrument: “B” shares. These were devised as a means for companies to return capital to shareholders. Typically a return of capital was more tax efficient for shareholders than dividends, and “B” shares were devised as a way for shareholders to choose the timing of this receipt – by reference to prearranged repayment dates – to mitigate their tax liability.

Most shareholders accepted their payment at the first opportunity, while some will have scheduled to accept it in a subsequent tax year. But a substantial minority didn’t want to get involved with the administration of a corporate action: the small size of many individual holdings made it more efficient to sell the shares in the market than pay the corporate action fee to accept the full payment. And some larger holders simply sold rather than bothering to look at the detail, assuming that the market bid would be close to fair value.

This assumption was false. We had become aware of “B” shares following one or two dealing enquiries, so we investigated. What we found interested us deeply. Firstly, although there was a growing number of this new type of shares, no single market maker covered them as a group: they were typically taken up, probably reluctantly, by market makers in the associated equity, as an add-on service for their customers. Secondly, the market was very uncompetitive. For example, WH Smith, an unexciting but perfectly sound company, had “B” shares in issue where the highest screen bid was 25p, but with a redemption offer by the company within a few months at 50p, offering a spectacular return for the buyer, and penalising anyone careless enough to passively accept the market bid.

We immediately registered as dealers in all the “B” shares we could identify. By covering the whole market and making sure our bid prices were (just) the best, we became the natural call for brokers with shares to sell. Once we acquired the shares, we could either book a healthy profit over a few months by holding them until redemption, or take an immediate turn by offering them to a client as a quasi-deposit investment, giving an attractive yield to redemption. This wheeze helped plug the gap in our profit and loss account for a couple of years.

By late 1999 Merrill Lynch’s chickens were coming home to roost. Their team’s strategy had been to make very large and close prices, while moving those prices steadily up – not difficult in a relatively small market, if you’re prepared to spend enough money buying stock. The combination of large holdings and rising prices appeared highly profitable, but this was unrealised profit, based on prices which they were controlling. A profit is only certain when the position is closed out. I couldn’t say whether Merrill paid their team bonuses based on these paper profits – it’s hard to believe they would have been so naïve, but who knows, large banks have made some very strange decisions over the years.

At any event, things must have come to a head. One day we came in to the news that Merrill had parted company with their fixed income team. They immediately stopped making prices in extravagant size – at least at the bid end – although their prices remained stubbornly high for a while, before easing slowly closer towards historically more typical levels.

I sensed they might have some unwinding to do, and over the next few months I got to know the softly spoken Scottish fellow who had been left in charge of Merrill’s preference positions. As I had hoped, one day he called us with some business: could we get a bid for 11.25 million NatWest 9%? In the sleepy backwater where I operated, I could usually only dream of getting an order like this. I made some calls and was able to find a buyer – albeit at a level below the prices displayed on screen – and Merrill accepted our bid. I had work to do: in the next few weeks I placed out tens of millions more of their shares with institutional investors.

Eventually the flow of this business dried up, as Merrill flattened their holdings, or at least reduced them to more comfortable levels. The screen prices were still unrealistically high, and we kept hearing reports of brokers and clients who were unable to execute their sell orders. This was an opportunity: anyone willing to make the right prices could potentially capture all the business. There were other market makers beside Merrill, but they were also compromised, presumably so long of stock that they would face heavy losses if they moved prices down to the true levels. Of course that was their problem, not ours.

We registered to once again make prices in the leading stocks. After some discussion, we opted for a wide ten point spread, bidding about fifteen points less than Merrill’s screen bid, offering at five points less, making prices in a princely 25,000. It was unusual (and bold) to publicly offer stock below their displayed bid price (called a backwardation) – we were effectively saying their prices were wrong.

The first day trading these stocks again was a nervous one. Our low prices looked out of line and initially attracted buyers: brokers came on to buy small amounts, checking that we were happy with the price – that is, we were happy to sell on a backwardation. “No problem” I replied, “We mean it, they don’t.” Easy to say, of course, but as the day went on our short positions steadily mounted at prices which, I was starting to worry, might be cheap. What if I had been wrong?

In the final hour of trading, relief arrived. A broker rang up with a few decent sell orders, seventy thousand of these, fifty thousand of those. “Are you happy with your bid prices?” he asked. “I’ve been trying to sell these for weeks, but no-one’s given me a bid for them.” I took all his stock and heaved a sigh of relief: we had filled our short positions, our prices had been validated, and we could carry on trading our levels with confidence.

Over the next weeks, our opposition implicitly acknowledged that we were right by slowly adjusting their prices down to our levels – one imagines this was not cheap – and some abandoned the preference market completely. It was a long time before we had any serious competition to worry about. Merrill, in particular would have suffered losses in clearing their positions which would horrify most firms, but which probably registered as a mere blip in their New York City headquarters.

Merrill’s aggressive and ultimately disastrous presence in the market, had come at some cost: my department’s profits had plummeted, and with it remuneration. This was uncomfortable at the time, although I had to remind myself that most people outside the City working in “real world” jobs – teachers, shopworkers, nurses – would still think my reduced pay very generous. And perhaps it was beneficial in the longer term: it left me with something still to prove. My appetite for business – and my enjoyment of it – stayed keen for many more years. The best years of my career were still ahead of me.

Over twenty-five years have passed since I had this unwanted close-up of a major investment bank in operation. And in case you’re wondering whether Merrill Lynch continued to make costly mistakes…oh yes. During the 2008 financial crisis they suffered huge losses from the drop in value of their mortgage portfolio of collateralized debt obligations, and they were forced to accept a takeover by Bank of America. I wasn’t too sad about that.

Leave a comment